5 A corporation shall not transfer shares held under subsection 4 to any person unless the corporation is satisfied on reasonable grounds that the ownership of the shares as a result of the transfer would assist the corporation or any of its affiliates or associates to achieve the purpose set out in subsection 4. The instrument of transfer of any share shall be executed by or on behalf of the transferor and transferee and the transferor shall be deemed to remain a holder of the share until the name of the transferee is entered in the.

2

Means the annual General Meeting of the Company held pursuant to section 125 of the Law.

. Introduction to sections 346 and 347. Instruments coming within several descriptions in Schedule ISubject to the provisions of the last preceding section an instrument so framed as to come within two or more of the descriptions in Schedule I shall where the duties chargeable thereunder are different be chargeable only with the highest of such duties. Transfer of field allowance.

B A term of years absolute. A transfer on death deed is revocable regardless of whether the deed or another instrument contains a contrary provision. Added by Acts 2015 84th Leg RS.

Relief after an exchange of shares for shares in another company. For purposes of determining income of the debtor from discharge of indebtedness to the extent provided in regulations prescribed by the Secretary the acquisition of outstanding indebtedness by a person bearing a relationship to the debtor specified in section 267b or 707b1 from a person who does not bear such a relationship to the debtor shall be treated as. 134 connection with the grant or transfer of a proprietary leasehold.

D A transfer on death deed transfers real property without covenant of warranty of. 150 be deemed to meet the requirements of paragraphs 2 and 3 of subdivision a of this section if 151 such shares are regularly quoted by dealers making a market in. TRANSFER OF SHARES.

Additional deduction under section 1149 of CTA 2009. No the transfer of shares between the ABCA business unit and the ABCB business unit to satisfy the customer order is not trade reportable because there is no change in beneficial ownership. Note that the sale to the customer must be reported for tape purposes.

Asset included in the total assets of a company that is a foreign. Part I EW General Principles as to Legal Estates Equitable Interests and Powers 1 Legal estates and equitable interests. D Except for provisions included pursuant to paragraphs a1 a2 a5 a6 b2 b5 b7 of this section and provisions included pursuant to paragraph a4 of this section specifying the classes number of shares and par value of shares a corporation other than a nonstock corporation is authorized to issue any provision of the certificate of incorporation.

2 The only interests or charges in or over land which are capable of. But theres an exemption available FRS 105 section 2810d. 3 seek under Section 33-44-8015 a judicial determination that it is equitable to dissolve and wind up the companys business.

Assessment day for an income year of a life insurance company has the meaning given by section 219- 45. Asset-based income tax regime has the meaning given by section 830- 105. Asset entity has the meaning given by section 12-436 in Schedule 1 to the Taxation Administration Act 1953.

F A limited liability company need not give effect to a transfer until it has notice of the transfer. The last surviving joint owner may revoke the transfer on death deed subject to Section 114057. Provided that nothing in this Act contained.

As used in NRS 78191 to 78307 inclusive unless the context otherwise requires the word distribution means a direct or indirect transfer of money or other property other than its own shares or the incurrence of indebtedness by a corporation to or for the benefit of all holders of shares of any one or more classes or series of the. EW 1 The only estates in land which are capable of subsisting or of being conveyed or created at law are a An estate in fee simple absolute in possession. 105 Subchapter it references a taxpayer and a non-taxpayer.

If the liability component isnt outstanding at the date of transition to. Obtaining Security Symbols for Trade Reporting. Tax credit under section 1151 of.

Chapter One And Two Shares And Shares Capital Topic One Shares Any Shareholder Or Studocu

Company Secretary Cosec Services Sdn Bhd Ipoh Mon T Kiara Kl C Highlands Penang

6 K 1 A19 5541 16k Htm 6 K United States Securities And Exchange Commission Washington D C 20549 Form 6 K Report Of Foreign Issuer Pursuant To Rule 13a 16 Or 15d 16 Of The Securities Exchange Act Of 1934

2

2

2

Media Chinese International Limited Form 32a Fill And Sign Printable Template Online Us Legal Forms

2

The Concept Of Transfer Of Beneficial Ownership Of Securities Azmi Associates

2

Malaysia Transmission Of Shares Universal Succession Conventus Law

Vishnu Manchu Sends Legal Notice To Voter Movie Director And Producer Gallery And Pdf Social News Xyz

2

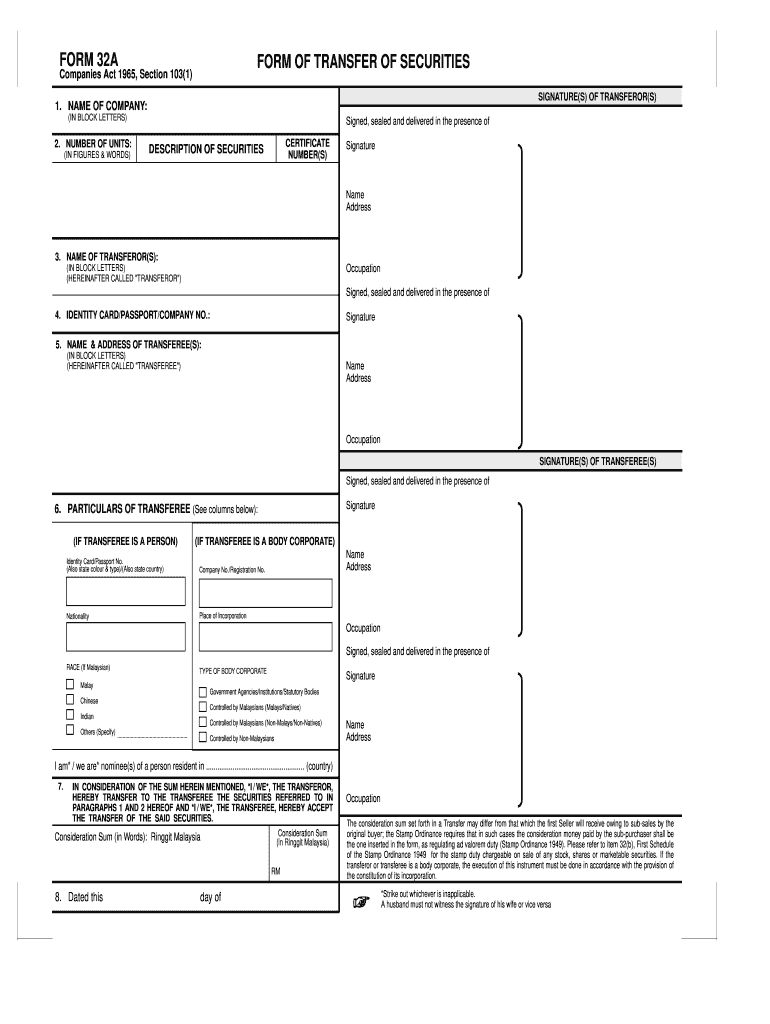

Section 105 Instrument Of Transfer Of Shares Tobyxvc

2

Section 105 Instrument Of Transfer Of Shares Tobyxvc

Tutorial 2 Asso 2 Syuhaidah Name Siti Nur Syuhaidah Binti Basir 2017678458 Group Lwb06j Studocu

Transfer Of Shares Malaysia Nashcxt

2

- income tax rate 2017 malaysia

- tips diet sehat dan cepat untuk remaja

- makna nama nazwa

- jay chou new song

- nota sains tingkatan 3 2019

- keahlian my umno org

- lukisan bunga cantik dan indah

- simpulan bahasa with chinese meaning

- taman dalam rumah kecil minimalis

- keputusan pru 14 dun semenyih

- undefined

- section 105 (instrument of transfer of shares)

- bra size letters in order

- gambar daun handeuleum

- ucapan selamat wisuda ke kakak

- jawatan kosong kerajaan kedah

- portal ppd pasir gudang

- kata kata melupakan mantan dalam bahasa inggris dan artinya

- tanjung rhu form 4 character

- karangan pendek bahasa melayu